How to Raise Your Credit Score

This post may contain affiliate links. Please read how we make money for more information.

We currently live in a world where having a good credit score matters – a lot. A bad score can really hold you back in life. Not only can it prevent you from obtaining credit for the things you need to buy, but it can also keep you from landing a good job.

Talk about a Catch-22!

Table of Contents

Why Do You Need a Good Credit Score?

Credit checks are done for just about all loans, whether it’s for an auto, home, or something else. Credit checks are even done by many cell phone carriers just to open an account.

It’s also now common for employers to run credit checks on potential job candidates. Many employers these days won’t hire applicants with low credit scores.

And to make matters even worse, many landlords now run credit checks on potential tenants before they will agree to rent to them. Without a good score, you may have trouble finding a decent place to live.

In short, a bad credit score can leave you without a good job, stuck in a bad neighborhood, and having to take the bus everywhere you go. It can totally ruin your whole day.

If you currently have a credit score that’s, shall we say, less than favorable, you may be tempted to throw your hands up in the air in despair. After all, there’s not much you can do about it, right?

Actually, there is.

As it turns out, there are some things you can do to improve your credit score. Keep in mind though that improving your score takes time. It doesn’t happen quickly.

Credit scores take into account years of financial activity, and turning things around is a process. It’s kind of like turning an aircraft carrier around in the ocean. Those big ships don’t turn on a dime. It takes a while for them just to make a u-turn. Likewise, it will also take a while to see changes to your credit score.

It’s also worth pointing out that some of these tips also apply if you are just getting started in life and you currently don’t have a credit score. Hey, everyone has to start somewhere, right?

If you are wondering how to raise your credit score, wonder no more. Here are a few things you can do:

1. Understand Your Credit Score

The first thing you can do to improve your credit score is to understand how credit reporting works. Knowledge is power, and if you want to turn things around, you first need to understand the basics.

First, a credit score is a three-digit number that is calculated based on a mix of your credit history and usage. Factors that contribute to your score include:

- Payment history (35%)

- New credit or credit inquiries (10%)

- How much debt you have vs available credit (debt usage) (30%)

- Different types of credit accounts (credit mix) (10%)

- Length of credit history (15%)

The higher your credit score, the better. Different organizations and credit reporting models have different ranges, but 300 to 850 is a common range.

2. Pay Your Bills on Time

It might seem like good common sense, but one of the best things you can do to improve your credit score is to simply pay your bills on time. This includes your credit cards, utilities, rent, any loans you may have, your monthly cell phone payment, and others.

It’s important to pay all of your bills on time even if it’s to a company that doesn’t report to the credit reporting agencies. The reason is simple – if you are in a situation where a collection agency is called in to take over your account on money you owe, the collection agency could report you to the credit reporting agencies, thus damaging to your credit score.

3. Don’t Carry Large Credit Card Balances

A major factor that credit reporting agencies use to determine your score is how much credit you are using compared to your total credit. This is referred to as your credit utilization ratio. This ratio is calculated by taking your total credit balance and dividing it by your total available credit (total buying power).

The less of your total available credit you use on a regular basis, the better it is for your credit score. If you do carry a balance on your credit cards from month-to-month, you can improve your credit score by paying down some of that balance and not adding any more to it. Ideally, you don’t want to tie up more than 30% of your available credit. Less is even better.

If you carry balances on more than one credit card, you might want to consider replacing that debt with a personal loan. Credit cards are notorious for charging high interest rates, so you may be able to save money in the long run by switching to a personal loan.

4. Be Careful with Hard Credit Checks

Are you currently in the market for a new car and you are applying to rent an apartment at the same time? Maybe you’re also thinking about refinancing your student loans.

Whoa. Easy there, tiger.

Whenever someone does a hard credit check on you, it can cause your credit score to go down. A hard credit check can stay on your credit report for up to two years.

A few sources of hard credit checks include:

- Auto loan applications

- Mortgage applications

- Credit card applications

- Personal loan applications

- Apartment rental applications

- Student loan applications

It’s important to point out that a hard credit check is different from a soft credit check.

What’s the difference?

Hard credit checks are generally done when a lending institution checks your credit to make a lending decision. Soft credit checks are typically those that are done for background checks. Unlike hard credit checks, soft credit checks do not hurt your credit score.

A few examples of soft credit checks include:

- Employment background checks

- Credit checks to rent an apartment

- Credit checks for insurance purposes

- Pre-qualified credit card offers

5. Don’t Worry About Old Debt on Your Report

Having old debt show up on your report isn’t necessarily a bad thing – so you don’t need to worry about having it removed. The exception to this, of course, is if there is an error on your credit report. If you ever see something on your credit report that you know is incorrect, you always want to dispute it.

Having a history of debt on your report where all of the payments were made on time actually helps your score, so you want to leave those things alone.

As a general rule of thumb, you want to leave any history of good payments on your credit report as long as possible. Yes, anything negative on your report will cause your score to go down, but it’s important to keep in mind that these things are typically removed from your report after a period of seven years. They eventually go away all by themselves.

6. Don’t Apply for More Credit Cards than You Actually Need

Many are tempted to apply for new credit cards when they get enticing offers in the mail. Maybe it’s a card with a really nice cashback rewards program or one that offers airline travel miles. Or perhaps it offers a super-low interest rate for an introductory period.

If you already have a couple of credit cards, opening a new account probably won’t help your credit score. In fact, it could have the opposite effect. There are some who will find it difficult not to use the new card to spend more, thus causing them to go deeper into debt.

7. Don’t Close Unused Credit Card Accounts

If you have one or more credit cards that you aren’t using and don’t think you’ll need again, you may be tempted to just close those accounts and cut up the cards. What’s the point in keeping them, right?

Keeping card accounts open that you aren’t using can actually benefit your credit score. That’s because closing an account could actually decrease the amount of available credit you have compared to the monthly balance you maintain. As previously mentioned, you don’t want to tie up more than 30% of your available credit.

This strategy may not make sense for you if you are currently paying an annual fee to keep your unused cards. It’s important to consider both the pros and cons of keeping these accounts open before making a decision.

8. Dispute Credit Report Errors

The three credit reporting agencies are Experian, TransUnion, and Equifax. You should periodically check your credit reports with all three agencies to see if there’s anything on them that shouldn’t be.

Sometimes things happen and inaccurate information can end up on your reports for a variety of reasons. If you see something on any of your reports that you know shouldn’t be there, you definitely want to dispute it with the agency reporting it.

Each of the three credit reporting agencies makes it very easy to open a dispute. You may be able to file a dispute online, by phone, or by mail. Information on filing a dispute is available online at each of the three credit reporting agency websites.

9. Negotiate with Creditors

If you end up with something negative on your credit report, it may be possible to have that black mark removed by negotiating directly with the creditor.

For example, if a credit card company tells the credit reporting agencies that you haven’t been paying your bills on time, you may be able to contact a representative from that company and strike a deal with them. You could offer to pay off all of your debt in exchange for them notifying the credit reporting agencies that the account has been “paid as agreed.”

There’s no guarantee that this will work for you, of course. It depends on your particular situation and the representative who receives your proposal. If a creditor does agree to strike a deal with you, be sure to get it in writing.

10. Set up a Payment Plan with Creditors

Many creditors will work with you if you aren’t able to pay down balances in-full or if you are having trouble making your minimum monthly payments.

Not all creditors are unreasonable ogres. The people you talk to about credit issues are human beings. And they realize that sometimes things happen and that occasionally people just need a little time to get things sorted out.

If you are struggling to make your payments on something, contact the creditor and ask them about setting up a payment plan. Creditors have a strong incentive to keep the money flowing and will often consider special payment arrangements. After all, being paid something each month is much better than receiving nothing at all.

With a special payment arrangement, you may be able to lower your monthly payments for a period of time. This could help you avoid late payments, which hurt your credit score.

If you do contact a creditor, just explain your situation and ask if they would consider a payment plan. Yes, it’s possible that the answer may be “no,” but It never hurts to ask.

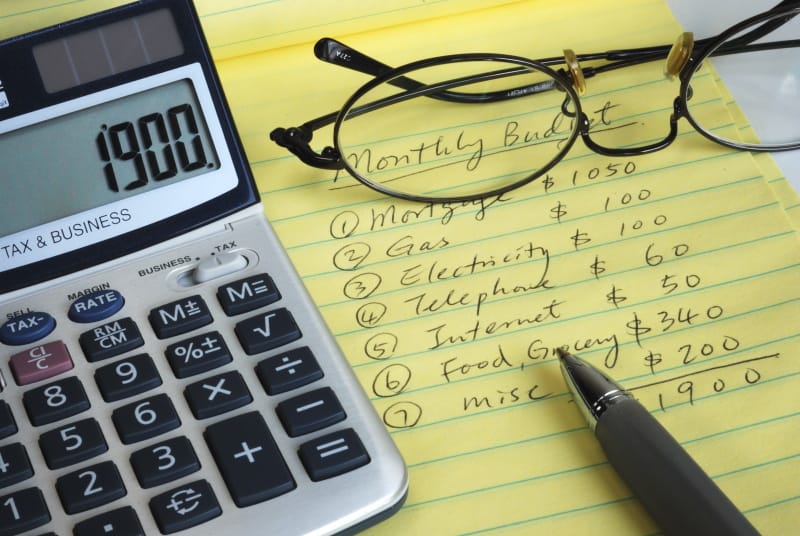

11. Live Within a Budget

If you are having a hard time making your monthly payments and you are concerned about having to make a few late payments, it may be time to create a budget.

A budget is a tool you can use to help you live within your means. It can help you find extra money you are currently spending on unnecessary things that you can put to better use – like paying down your debt.

Creating a budget isn’t a difficult task. You just want to set aside a couple of hours of your time to make a list of all of your necessary monthly expenses and then compare your list to your current income.

One of the great things about making a list of expenses is that it forces you to consider whether you really need everything you are currently buying each month. Maybe it’s time to cut the cord, for example, and stream free television content over the internet. Or maybe you could save a lot of money by cutting some bad habits out of your life – like alcohol and tobacco products.

12. Make Additional Credit Card Payments

Using too much of your available credit limit can negatively impact your credit utilization ratio. If you’ll recall, I previously mentioned that you don’t want to use more than 30% of your available credit at any given time.

But what happens if you have an emergency and need to use your credit card?

Things happen. Sometimes extra expenses come our way that we didn’t plan on and couldn’t have foreseen. Perhaps it’s a medical expense, or your car suddenly needs an expensive repair, or maybe the pipes in your basement burst and flooded your home. Whatever it is, you have to put it on your credit card.

If you suddenly end up with extra expenses on your credit card, you might want to consider making an additional payment in the middle of a billing cycle to reduce the total amount due and to free up some of your credit before it negatively impacts your credit rating.

13. Ask for a Credit Limit Increase

Another strategy you can use to raise your credit score is to contact a rep with one of your credit cards and ask them to increase your credit limit. The purpose of the credit increase is to give you a more favorable credit utilization ratio.

You have to be careful with this if you tend to overspend when you have more available credit. Naturally, this strategy isn’t going to work if your card company grants you a credit increase and you then buy a bunch of extra stuff. Self-restraint is needed.

There’s another caveat to this strategy that you need to be aware of. If you’ve recently missed a few payments or if your credit score is downward trending, your request for a credit limit increase may be denied.

And to make matters worse, it’s possible that the person reviewing your credit card account may actually decide to decrease your credit limit after reviewing your payment history. Yes, it’s possible this may backfire on you.

Nevertheless, if you’ve got a good payment history and you’ve been with a card company for a few years, you may be able to have your credit limit increased just by asking. If you request a credit limit increase, have a specific amount in mind when you ask.

14. Get Added as an Authorized User

Another strategy you can use to raise your credit score is to get added as an authorized user to another person’s credit card account. You will most likely have to ask close friends or family members – most people will not consider adding you if they don’t know you well.

If you are added as an authorized user to someone’s credit card account, you will receive a card with your name on it to make purchases.

The great thing about this strategy is that even though you are not the primary account holder, you still get to benefit from being associated with a credit card account with a good payment history.

This can be beneficial to you even if the person who allows you to be an authorized user on his or her credit card account doesn’t actually give you a credit card. Just being associated with the account is often enough to help your own credit rating.

If you want to try this strategy, it’s vitally important that you become an authorized user on an account with a good payment history. You do want to be picky about who you choose.

You want to be associated with an account that has a solid payment history with a low balance. It’s also beneficial for the account to be established – one that has been open for a while – and not one that is relatively new.

15. Consider Taking out a Secured Credit Card

If you have poor credit or you currently don’t have any credit, you might have some trouble acquiring a credit card. It’s a Catch-22, right?

How can you prove you are credit-worthy if you don’t have a way of acquiring credit to show you can make payments on time?

There is a way to acquire a credit card to help build your credit, but there is a bit of a catch to it. It involves taking out a secured credit card.

What’s a secured credit card?

A secured credit card is usually obtained from a bank or credit union. It requires you to make a deposit with the lending institution to cover the credit line you will receive from them. For example, if you want a credit card with a $500 limit, you will have to deposit $500.

Lending institutions usually have no problem issuing secured credit cards because you are making a deposit to cover the line of credit. And when you finally decide to close your account, you get your deposit back.

If you do decide to check with a lending institution about obtaining a secured credit card, it’s important to make sure they do report your on-time payments to the three credit reporting agencies. The primary purpose of acquiring one of these cards, after all, is to help build your credit rating.

If you already have a credit card, you don’t need to obtain a secured credit card. This strategy is for those who currently don’t have a credit card due to a poor credit history or they are just getting started in life and don’t have any credit history at all.

16. Consider Applying for a Student Credit Card

Another option to consider if you currently don’t have a credit card due to having a poor credit history or you are just starting out in life and you need to build your credit is to apply for a student credit card. As the name implies though, you do typically have to be a college student to qualify for one.

The main benefit of obtaining a student credit card is that they are usually easier to qualify for than regular credit cards. They usually don’t have very high income requirements. But on the other hand, they also usually don’t have very high lines of credit.

Student credit cards are great for small purchases, like fuel for your car, the occasional meal or snack, school supplies, and similar things. As with all credit cards, building your credit depends on making regular monthly payments before the due dates.

17. Consider Taking out a Credit Builder Loan

Here is another strategy for building your credit score if you have bad credit or you currently don’t have a credit rating because you are just starting out in life. The strategy involves taking out and repaying a small loan from a bank or credit union. These loans are often referred to as credit builder loans.

When you talk to a loan officer about why you want the loan, it’s best to be completely truthful. Just explain that you are interested in doing this to help build your credit. Most loan officers are familiar with credit builder loans.

The amount you take out doesn’t have to be very high. You could, for instance, take out a small $1,000 loan and repay it over a period of one year. The purpose of the loan is simply to make on-time payments each month long enough for the payments to be reported to the credit reporting agencies.

When you take out a credit builder loan, you will be required to put down a deposit with the bank for the full amount of the loan. The money is then placed in a savings account (which you will not be able to access).

A credit builder loan is very similar to obtaining a secured credit card. Instead of obtaining a credit card, however, you’ll be obtaining a regular loan with fixed monthly payments.

In order for the loan arrangement to work, you will have to deposit all of the loan amount with the bank. So, if you are taking out a $1,000 loan, you will have to deposit $1,000.

If you do encounter a situation where your bank or credit union does not make credit builder loans, just shop around. Some banks do and some don’t.

18. Earn More Money

Ideally, you don’t want to use more than 30% of your available credit at a time. If you go over that amount, you definitely want to pay it down as soon as possible so it doesn’t negatively affect your credit score. And in a perfect world, it’s really best to pay your credit card balances in full each month.

But how do you do that if your paycheck barely covers everything as it is?

You work more. You either take on a second job or you pick up a side-hustle. Where there’s a will, there’s a way.

There are several ways to earn money on the side that you can do during your free time. You could start a part-time business, for example. Many people enjoy their side hustles so much they end up ditching their jobs to go into business full-time for themselves.

A few examples of work-from-home jobs and businesses you can start for very little money include:

- Freelance writing

- Selling products on Amazon

- Starting a blog

- Starting an online store

- Being a virtual assistant

- Being a proofreader

- Being a virtual bookkeeper

- Teaching English online

- Flipping products on eBay

19. Continue Making Steady Progress

If you find that you are getting close to your desired score but you still aren’t quite there yet, don’t give up. It’s important to develop good habits that lead to a high credit score and to continue doing those things until your score improves.

And it will eventually turn around. No one can say with certainty how long it will take though. It’s also important to remember that negative things on your credit report typically stay there for at least seven years, including bankruptcies. These things don’t disappear overnight.

Improving your credit score is definitely possible, but you have to approach it with the understanding that it’s going to take a while to see results, even if you are doing everything right.

A good credit score can unlock many doors in your life. And by developing good financial habits, you can improve your score to land a new job, rent a better home, and do many other things.